Abstract

1. Introduction

We test five hypotheses: (H1) social metric growth predicts market cap growth; (H2) some metrics are stronger predictors; (H3) effects are stronger for smaller coins; (H4) short-term dynamics are better captured; (H5) aggregate social metrics co-move with market direction. Our findings challenge the simple narrative that “more followers means higher prices” and reveal a more nuanced picture.

2. Data

Table 1. Variables, coverage, medians, and cross-sectional Spearman rank correlations with log(market cap). All ρ significant at p<0.001. Telegram Subscribers has 58% missingness, limiting inference for this metric.

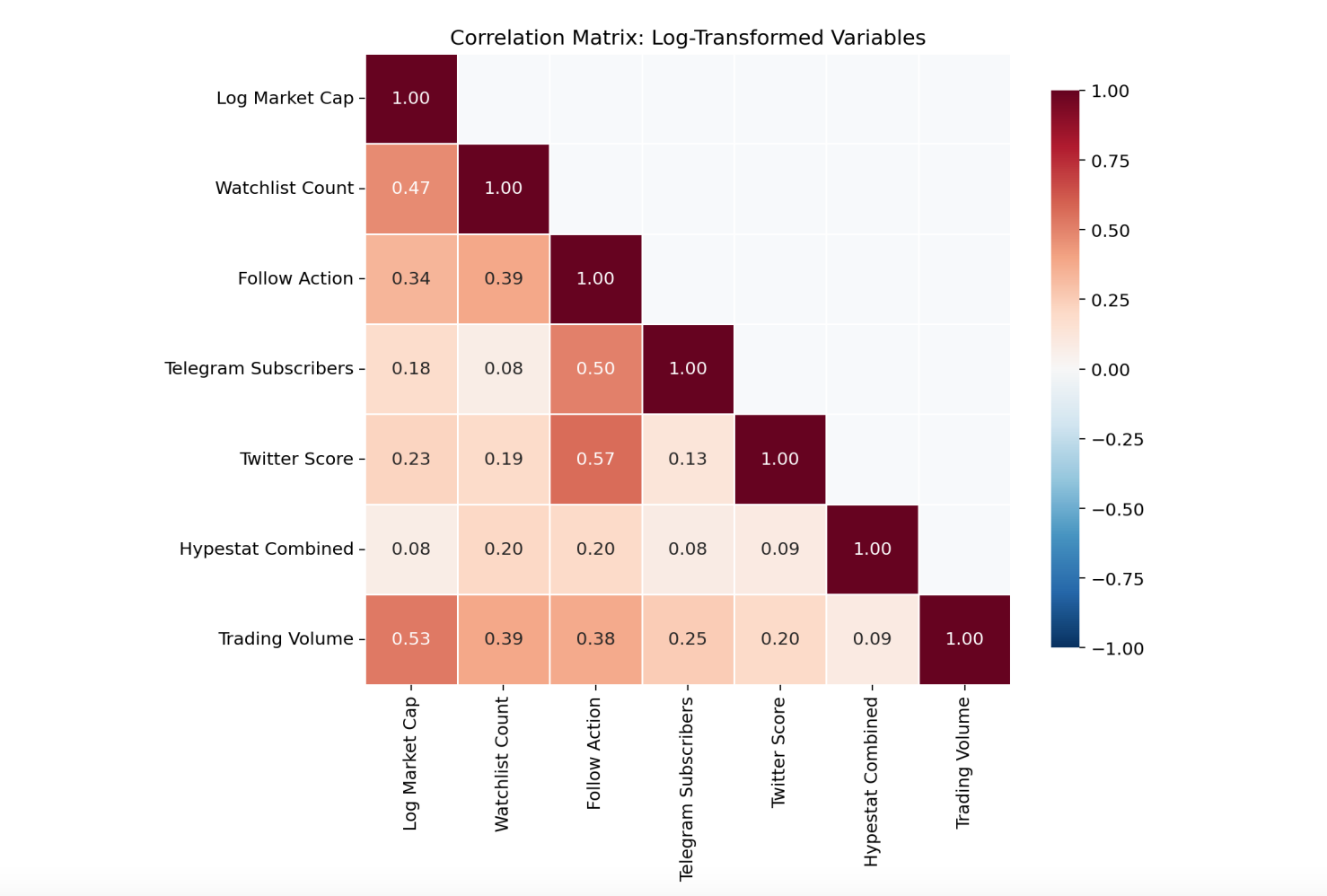

Figure 1. Pairwise correlations among log-transformed variables. Trading Volume and Watchlist Count show the strongest level-association with market capitalization.

3. Methodology

fwd_reti,t(h) = αi + γt + β · ∆log_metrici,t + εi,t

The lagged specification includes metric lags t−1 through t−4:

fwd_reti,t(h) = αi + γt + Σk=1..4 βk · ∆log_metrici,t−k + εi,t

where α i absorbs time-invariant coin characteristics and γ t absorbs common market shocks. Standard errors are clustered at the entity level. We use entity-level (rather than two-way) clustering because the number of time periods (T=91) is large relative to typical panel-FE applications, but we acknowledge that two-way clustering could be a stricter alternative.

We estimate both separate-metric and joint (all variables) models across horizons h=1..4. For market-level analysis (H5), we use OLS with Newey-West HAC standard errors (3 lags). Robustness checks: entity-FE only, time-FE only, winsorization (1st/99th percentile), excluding top-10 coins, and sub-period splits (first vs. second half).

4. Results

Table 2 reports separate-metric two-way FE results at h=1. Trading Volume achieves significance (p=0.003) but with a negative coefficient, consistent with a mean-reversion interpretation: volume spikes tend to precede weaker subsequent performance. Twitter Score is marginally significant (p=0.029) with a positive but economically negligible coefficient. Within-R2 is below 0.2% in all cases, indicating that social metric changes explain virtually none of the within-coin return variation after absorbing fixed effects. H1 is not supported at the panel level.

Table 2. Separate-metric two-way FE regressions, h=1. Dependent variable: forward log-return. Entity-clustered SE. *** p<0.001, ** p<0.01, * p<0.05.

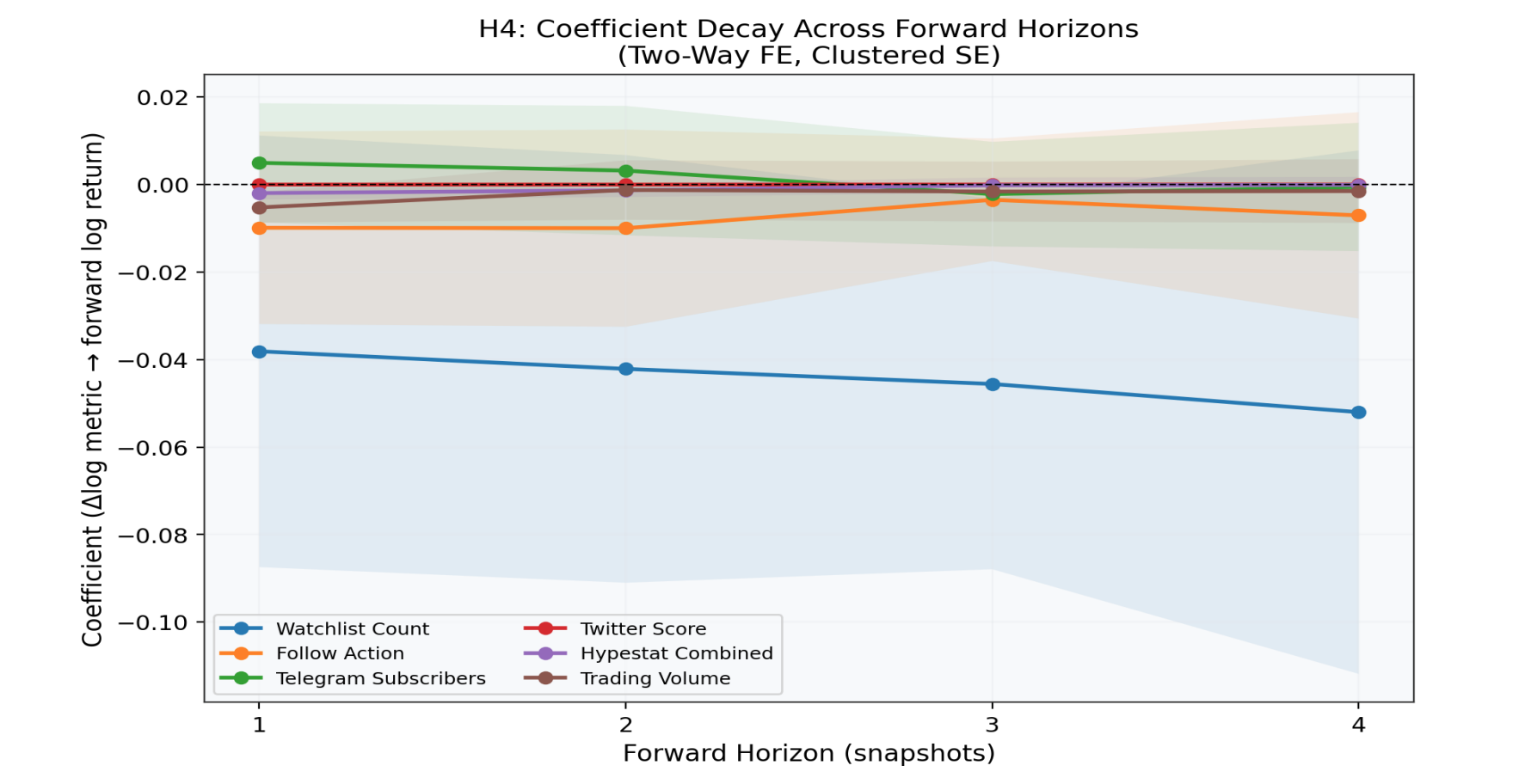

Figure 2. Coefficient estimates across h=1..4 (separate-metric models, 95% CI shaded). Effects dissipate beyond h=1 for Trading Volume. Watchlist Count shows a persistent negative pattern consistent with delayed reversal

Table 3. Size-bucket joint FE regressions. Full results for all metrics and both horizons. Significance: *** p<0.001, ** p<0.01, * p<0.05, + p<0.1.

Table 4. Market-level OLS: ∆log(total mcap) on ∆log(mean metric). Newey-West HAC SE (3 lags). 5 snapshots with missing mcap data excluded.

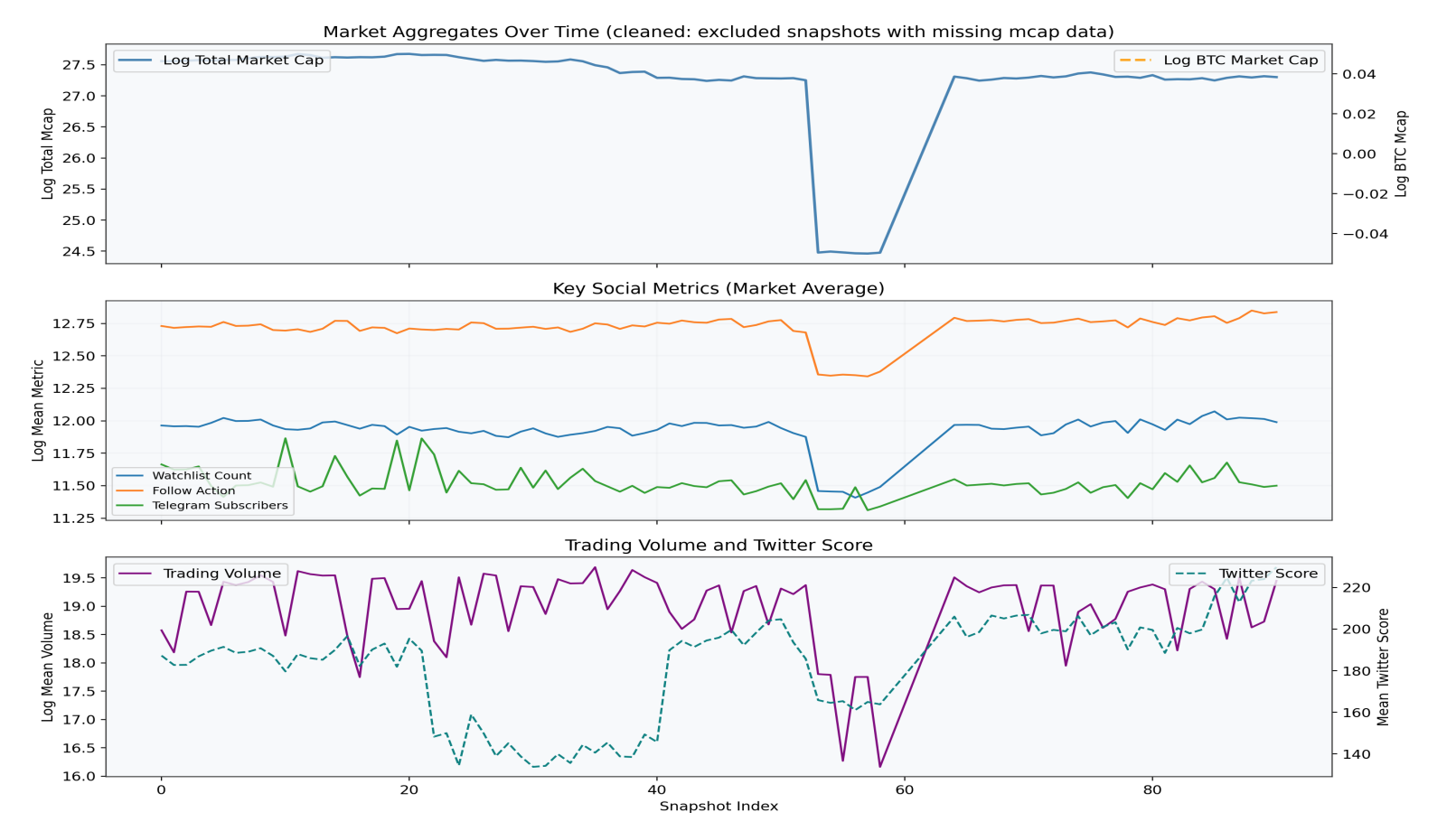

Figure 3. Market aggregates over time (5 broken snapshots excluded). Top: total and BTC market cap with regime shading. Middle: mean social metrics. Bottom: trading volume and Twitter Score.

Table 5. Robustness summary at h=1. The sub-period instability of Twitter Score (p=0.0001 vs. p=0.233) indicates that its baseline significance is driven by a specific market episode in the first half, not a stable structural relationship.